Können Sie mich gut sehen und verstehen?

Ja NeinVielen Dank. Wir freuen uns, Sie hier in Kürze wieder begrüßen zu dürfen.

- Geld kann im Ruhestand knapp sein

- Ihr Arbeitgeber unterstützt bei Aufbau zusätzlicher Rente

- Rente zum Nulltarif, ohne Einsatz eigenen Geldes

Teil 1

Allgemeine Informationen zur gesetzlichen Rente

Teil 2

Ihr persönliches Angebot zur Rente zum Nulltarif

Teil 3

Zusammenfassung Dokumentation für Sie und Ihren Arbeitgeber

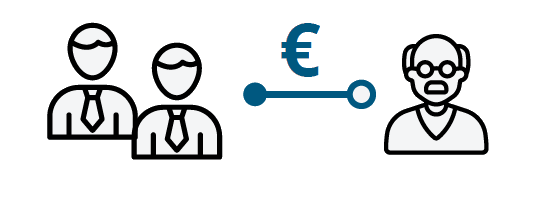

Situation der gesetzlichen Rente

Heute:

2 Arbeitnehmer finanzieren Rente eines Rentners

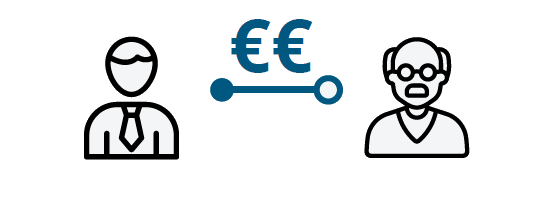

Zukunft:

1 Arbeitnehmer finanziert Rente eines Rentners

Das bleibt nicht ohne Auswirkungen…

Internetpauschale

50,00 €

Steuer- und Sozialversicherungs-Ersparnis

43,31 €

Ihr Gesamtbeitrag

90,00 €

Ihre einmalige Kapitalleistung zu Rentenbeginn

49.211,23 €

* unverbindliches, schematisches Beispiel, mit gerundeten Werten

Schade, aber selbstverständlich wollen wir auch Ihnen ein Angebot machen. Dürfen wir Sie dazu telefonisch kontaktieren? Bitte nennen Sie uns Ihren Namen und eine Telefonnummer, unter der wir Sie erreichen können. Alternativ können Sie sich auch an Ihre Personalabteilung wenden.

Ja, bitte kontaktieren Sie mich:

Vielen Dank. Wir werden uns in Kürze telefonisch mit Ihnen in Verbindung setzen.

Vielen Dank. Wir freuen uns, Sie hier in Kürze wieder begrüßen zu dürfen.

Laut unseren Unterlagen haben Sie bereits teilgenommen. Sollte dies ein Fehler sein, kontaktieren Sie uns bitte unter support@renteundmehr.de oder Telefon +49 28 71 / 27 71 - 33

Ihr Geld ist sicher

Absicherung mit eigenem Versorgungswerk

- gesetzlich geregelte Versorgungsordnung

- Entscheidender Vorteil gegenüber Betriebsrente über eine klassische Versicherung

100% Insolvenzschutz

gesetzlich garantiert

Pensions-Sicherungs-Verein

Ihre Betriebsrente ist insolvenzgeschützt

Teil 1

Allgemeine Informationen zur gesetzlichen Rente

Teil 2

Ihr persönliches Angebot zur Rente zum Nulltarif

Teil 3

Zusammenfassung Dokumentation für Sie und Ihren Arbeitgeber

Das sollte natürlich nicht sein. Dürfen wir Sie dazu kontaktieren? Bitte nennen Sie uns Ihren Namen und eine Telefonnummer, unter der wir Sie erreichen können. Alternativ können Sie sich auch an Ihre Personalabteilung wenden.

Ja, bitte kontaktieren Sie mich:

Vielen Dank. Wir werden uns in Kürze telefonisch mit Ihnen in Verbindung setzen.

Vielen Dank. Wir freuen uns, Sie hier in Kürze wieder begrüßen zu dürfen.

Ihre Rente zum Nulltarif

Internetpauschale

50,00 €

Steuer- und Sozialversicherungs-Ersparnis

€

Ihr Gesamtbeitrag*

,00 €

Ihre einmalige Kapitalleistung zu Rentenbeginn

€

Bauen Sie sich Ihr Rentenkapital zum Nulltarif aus.

Schritt 1

Schritt 2

Schritt 3

Schritt 4

Schritt 5

Internetpauschale

- + 600 € pro Jahr

- Brutto = Netto

% Zins

- 100% Garantie

- 100% Insolvenzschutz

Ihre Kapitalleistung

- €

- Ihr Netto bleibt gleich

Bitte laden Sie die Dokumente durch Klick auf das Download-Symbol herunter, lesen Sie sie sorgfältig durch und bestätigen Sie mit Klick auf die Checkbox, dass sie alles gelesen und akzeptiert haben. Klicken Sie danach auf Weiter.

Folgende Dokumente sind enthalten:

- Beratungsdokumentation

- Ergänzende Vereinbarung

- Entgeltumwandlungsvereinbarung

- Versorgungszusage

For legal reasons, all documents are written in German.

gelesen und akzeptiert